Introduction: The Morning Everything Changed

It was a perfectly ordinary Wednesday morning.

Jennifer, 38 years old, woke up feeling slightly off. A little chest tightness. Some shortness of breath. She figured it was stress — work had been hectic lately, she had not been sleeping well, and she had skipped the gym for three weeks straight. She drank her coffee, got dressed, and was halfway to her car when the pain hit her properly.

Four hours later she was in a hospital bed. Cardiac event. Serious but survivable. The doctors were excellent. The care was exceptional. The treatment worked.

Three weeks after discharge, the bill arrived.

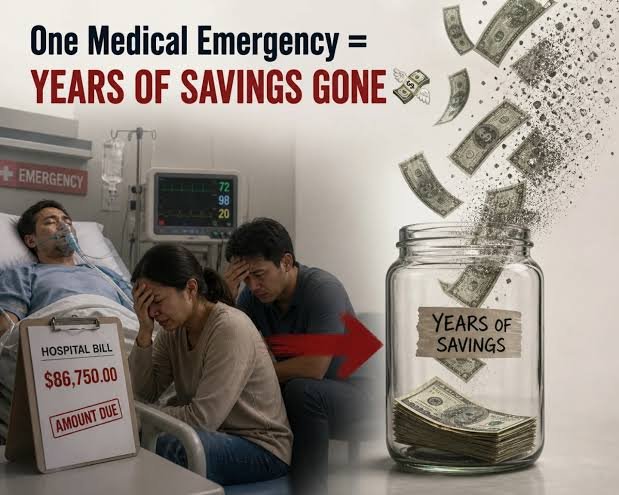

$94,000.

Jennifer and her husband Mark had spent eleven years building their savings. They had been disciplined, careful, intentional about money. They had $61,000 saved — their emergency fund, their house deposit, their retirement starter, their security blanket built through years of sacrifice and sensible decisions.

It was gone in a single payment. And they still owed $33,000 more.

They had always meant to sort out proper health insurance. They had a basic plan through Jennifer’s employer, but they had never upgraded it, never really read what it covered, never thought seriously about whether it was actually enough. It felt like one of those things you deal with properly later.

Later arrived on a Wednesday morning without any warning at all.

This Is Not a Rare Story

Before we go any further, let us be completely honest about something important.

Jennifer and Mark’s story is not unusual. It is not a rare worst-case scenario that happens to one unlucky family in a million. It is one of the most common financial disasters that happens to ordinary, hardworking, responsible people every single year in countries around the world.

Medical debt is consistently ranked as one of the leading causes of personal bankruptcy. In the United States alone, studies have shown that medical expenses contribute to a significant percentage of all bankruptcy filings — and the majority of those people had some form of health insurance. They just did not have the right health insurance, or enough of it.

In countries with public healthcare systems, the situation looks different on the surface but the core problem remains. Waiting lists, limited coverage for certain treatments, private specialist fees, prescription costs, rehabilitation expenses, lost income during recovery — the financial impact of serious illness reaches far beyond what most people anticipate.

The families who get through serious medical events without financial devastation are not luckier than the ones who do not. They are simply better prepared.

Why People Gamble With Their Health Coverage

Let us talk honestly about why so many intelligent people end up dangerously underinsured when it comes to their health. Because the reasons are completely understandable — even if the consequences are severe.

“I’m healthy. I never really use it.”

This is probably the single most common reason people skimp on health insurance. When you are feeling well, paying significant premiums for coverage you barely use feels wasteful. It feels like throwing money away every month for something you do not actually need.

This logic has one catastrophic flaw: health insurance is not for the healthy version of you today. It is for the sick version of you tomorrow — the version you cannot predict, cannot schedule, and cannot prepare for in any other way.

“Healthcare costs can’t really be that high.”

Until you have personally received a serious medical bill, the numbers are genuinely difficult to believe. People have a vague sense that hospitals are expensive, but the reality of modern medical costs — ICU stays, surgical procedures, specialist consultations, diagnostic imaging, medication, rehabilitation — is something that has to be experienced to be truly understood.

A single night in an intensive care unit in the United States can cost between $10,000 and $20,000. A complex surgery can run $50,000 to $150,000 or more. A cancer diagnosis and treatment course can easily reach $500,000 over several years. These are not extreme outliers. These are standard costs for standard serious medical events.

“I’ll sort out better coverage next year during open enrollment.”

Open enrollment periods create a dangerous psychological trap. There is always a next enrollment period coming. There is always a slightly better time to upgrade, reconsider, or actually sit down and read through the options properly. Meanwhile the current inadequate coverage stays in place month after month, year after year.

“The premium savings help my budget right now.”

Choosing a lower-premium, higher-deductible plan to save money each month is a perfectly rational decision for healthy young people with significant savings — provided they actually have the savings to cover that deductible if something goes wrong. The problem is that most people who choose low-premium plans do so specifically because money is tight, which means they also do not have the savings cushion to handle a large deductible. It is a financial trap that is very easy to fall into.

“My employer’s plan is fine.”

Employer health plans vary enormously in quality and coverage. Some are excellent. Many are adequate. Some are genuinely insufficient. But because it feels like a benefit — something being given to you rather than something you are choosing — people rarely scrutinise employer health plans with the same attention they would give to a plan they were selecting and paying for themselves.

The True Cost of a Medical Emergency Without Proper Coverage

People think about health insurance costs in terms of monthly premiums. They compare plans by looking at what they pay each month. This is the wrong way to think about it.

The right question is not: what does this insurance cost me?

The right question is: what does a serious medical event cost me without proper insurance?

Let us walk through a realistic scenario in detail.

Imagine you are 35 years old. You are reasonably healthy. You have a basic insurance plan with a high deductible because the monthly premiums are lower and you have not had any serious health issues.

One afternoon you experience symptoms that turn out to be appendicitis. This is not a dramatic, unusual illness. Appendicitis is one of the most common surgical emergencies. It happens to ordinary people all the time.

Here is what your costs might look like:

Emergency room visit and initial assessment — potentially $2,000 to $3,000. Diagnostic imaging including CT scan — $1,000 to $3,000. Emergency appendectomy surgery — $15,000 to $30,000. Anaesthesiology fees, which are often billed separately — $2,000 to $5,000. Hospital stay of one to three days — $5,000 to $15,000 per day. Prescription medications — several hundred dollars. Follow-up appointments — additional hundreds to thousands.

Total for a routine appendectomy: easily $25,000 to $50,000 before your insurance even begins covering the significant portion, depending on your deductible and out-of-pocket maximum.

Now imagine not appendicitis but something more serious. A car accident. A stroke. A cancer diagnosis. A heart condition requiring ongoing management. The numbers grow very quickly into territory that can destroy decades of careful financial planning in a single event.

The Hidden Costs Nobody Warns You About

Hospital bills are the obvious financial impact of a serious illness. But they are far from the only one. People who have lived through major medical events describe a whole ecosystem of costs that they never anticipated.

Lost Income

Depending on your employment situation and the severity of your illness, you may be unable to work for weeks, months, or even permanently. For self-employed people or those without adequate sick pay provisions, this income loss begins immediately. Even for people with good sick pay, extended illness often eventually leads to reduced pay or the need to take unpaid leave.

A health insurance plan with income protection components, or a separate income protection policy, is something that most people never consider until they desperately need it.

The Cost of Recovery

Serious illnesses and injuries often require extensive recovery periods that come with their own significant costs. Physical therapy and rehabilitation, occupational therapy, home modifications if mobility is affected, specialist follow-up appointments, ongoing prescriptions — none of these are optional extras. They are essential parts of getting back to health and function.

Many basic health insurance plans cover acute treatment adequately but provide limited support for the recovery phase that follows. This gap catches people completely off guard.

Mental Health Impact and Its Costs

A serious medical event does not just affect your body. The psychological impact of a significant illness or injury — anxiety, depression, post-traumatic stress, fear of recurrence — is well documented and very real. Mental health treatment, therapy, and in some cases psychiatric medication add another layer of expense that basic insurance plans often cover poorly or not at all.

The Family Ripple Effect

When one person in a family becomes seriously ill, the financial impact radiates outward. A partner may need to reduce their working hours to provide care. Children’s activities and opportunities may be affected. Families may need to hire help they never previously needed. The household budget that was built around two functioning, earning adults suddenly has to absorb both reduced income and increased expenses simultaneously.

Real Stories, Real Numbers

Beyond Jennifer and Mark, here are the kinds of stories that play out in real families every single year.

The Self-Employed Freelancer

Tom ran his own graphic design business. He was 41, fit, active, and had let his health insurance lapse during a lean period two years earlier, always intending to sort it out when things picked up financially. He was diagnosed with Type 2 diabetes — manageable, treatable, but requiring ongoing medication, regular specialist appointments, and monitoring equipment. Without insurance, his monthly management costs ran to nearly $800. Over a year that is close to $10,000 in health expenses alone, on top of everything else. His business nearly collapsed under the weight of it.

The Young Family

Rachel and David had their first baby at 32. They had chosen a high-deductible health plan to keep monthly costs down during the pregnancy — a reasonable decision that seemed sensible at the time. Their baby was born six weeks premature and required three weeks in the neonatal intensive care unit. The NICU costs alone exceeded $150,000. Their share after insurance was still $18,000 — money they simply did not have. They spent the next four years paying off medical debt during what should have been the most exciting period of their lives.

The “Healthy” 29-Year-Old

Sophie had been uninsured for two years after leaving a job that provided coverage. She was young, she felt invincible, and the premium costs felt unjustifiable on her modest salary. A routine sports injury that seemed minor turned out to require surgery and rehabilitation. The total bill: $34,000. She had nothing close to that in savings. The debt followed her for years, affecting her credit score, her ability to rent an apartment, and her stress levels every single day.

What Good Health Insurance Actually Looks Like

Understanding why health insurance matters is the first step. Understanding what adequate health insurance actually looks like is the step that protects you.

Coverage That Matches Your Real Risk

A good health insurance plan should cover hospitalisation comprehensively — not just basic admission but surgical procedures, specialist consultations, intensive care, and extended stays. It should cover emergency care without creating financial shock through excessive cost-sharing at exactly the moment you are most vulnerable.

Manageable Deductibles and Out-of-Pocket Maximums

The deductible is what you pay before insurance kicks in. The out-of-pocket maximum is the most you will pay in a given year even in a catastrophic scenario. These two numbers are arguably more important than your monthly premium because they determine your actual financial exposure when something goes wrong.

A plan with a $200 monthly premium and a $8,000 deductible is not cheaper than a plan with a $400 monthly premium and a $2,000 deductible — not when you actually need to use it.

Prescription Drug Coverage

Medications for chronic conditions are ongoing, non-negotiable expenses. A plan that covers prescription drugs adequately can save thousands of dollars annually for anyone managing a chronic condition. Check this carefully before selecting any plan.

Mental Health Coverage

Given what we know about the mental health impact of serious illness, injury, and the general stresses of modern life, mental health coverage deserves specific attention when evaluating any health insurance plan. Adequate therapy coverage, psychiatric coverage if needed, and substance abuse treatment are important components of genuinely comprehensive health coverage.

Preventive Care

The best health outcome is one where serious illness is caught early or prevented entirely. Plans that cover preventive screenings, vaccinations, annual check-ups, and early intervention services are not just being generous — they are being financially smart. Catching a condition early is dramatically cheaper for everyone than treating it after it has progressed.

The Preventive Power of Health Insurance

Here is something that often gets lost in conversations about health insurance: it is not just a financial tool for when things go wrong. It is actively a health tool that can prevent things from going wrong in the first place.

People with good health insurance use it. They go for their annual check-ups. They get the screening their doctor recommends. They do not delay seeing a specialist when something does not feel right. They fill their prescriptions and take their medication consistently.

People without adequate health insurance delay care. They skip check-ups to avoid costs. They wait to see if symptoms resolve on their own. They avoid specialist referrals. They sometimes cut medication doses to make prescriptions last longer.

These are not irresponsible decisions — they are rational responses to financial pressure. But they have consequences. Conditions that are caught early are treated more successfully, less expensively, and with better long-term outcomes than conditions that are caught after years of being ignored.

Health insurance is not just protection against financial catastrophe. It is an investment in actually staying healthier across your entire life.

How to Choose the Right Health Insurance Plan

Choosing health insurance can feel overwhelming, especially when you are staring at a comparison table full of numbers, percentages, and terminology that feels deliberately confusing. Here is a straightforward framework for making a good decision.

Step 1: Be Honest About Your Health and Your Risk

Start by honestly assessing your current health situation and your family’s health history. Do you manage any chronic conditions? Does your family have a history of heart disease, cancer, or other significant conditions? Do you have children who are active and occasionally injury-prone? Your answers shape what coverage level genuinely makes sense for you.

Step 2: Calculate Your Real Total Cost

Do not compare plans by monthly premium alone. For each plan you are considering, work out the realistic total annual cost including premiums, likely out-of-pocket costs based on your typical healthcare usage, and your maximum exposure in a worst-case scenario. This complete picture often changes which plan looks most sensible.

Step 3: Check Your Preferred Doctors and Hospitals

If you have existing doctors you trust or specialists you see regularly, check that they are in-network for any plan you are considering. Receiving care out-of-network can dramatically increase your costs and in some cases mean your insurance barely contributes at all.

Step 4: Understand What Is Actually Covered

Read the coverage details properly. Know what requires pre-authorisation. Understand what your plan considers preventive care versus treatment. Know the mental health coverage. Know the prescription drug formulary. Insurance policies are detailed documents for a reason — the details matter enormously.

Step 5: Review Annually

Your health situation, your family situation, and the insurance options available to you all change over time. What was the right plan at 28 and single may not be the right plan at 36 with a family. Annual review of your coverage is not excessive — it is responsible.

The Conversation About Money and Health

There is a cultural awkwardness around discussing healthcare costs and health insurance. It touches on our mortality, our vulnerability, and our financial situation all at once — a combination that most people find deeply uncomfortable.

But avoiding that conversation is exactly how families end up in Jennifer and Mark’s situation. Stunned, scared, and watching years of careful saving disappear because they never properly confronted the reality of what medical costs actually look like.

Have the conversation with your partner. Have it with your parents if they are getting older and may need your support navigating healthcare decisions. Have it with yourself honestly if you have been putting off looking at your current coverage properly.

The conversation is uncomfortable for about twenty minutes. The financial devastation of being inadequately insured can last for years.

What Jennifer and Mark Did Next

It would be wrong to end their story at the lowest point.

Jennifer and Mark rebuilt. It took four years. It was genuinely hard, and there were months where the stress between them was almost unbearable. But they got through it.

And the very first thing they did after the initial medical crisis was resolved was sit down together and go through every insurance policy they had. Life insurance. Health insurance. Income protection. They did it properly this time — with a financial advisor, with a real understanding of what they were buying, and with complete honesty about what they could afford and what they needed.

Their monthly insurance costs went up. But Jennifer told the story this way: “Every month when I see that premium come out of our account, I feel relief, not frustration. Because I know what the alternative looks like now. I’ve lived it.”

That shift in perspective — from seeing insurance as an annoying expense to seeing it as an essential foundation — is something that unfortunately often comes only after experiencing firsthand what insufficient coverage costs.

The goal of this article is to help you make that shift without having to learn it the hard way.

The Bottom Line

One hospital bill wiped out Jennifer and Mark’s entire savings. Not because they were careless people. Not because they were financially irresponsible. But because they had never genuinely confronted the gap between the coverage they had and the coverage they actually needed.

That gap is silent. It costs nothing until suddenly it costs everything.

Health insurance is not a luxury. It is not something you sort out when you have more money, more time, or a more convenient moment. It is the financial foundation that allows everything else in your life to remain standing when the completely unexpected — and it is always unexpected — arrives.

Your savings deserve protection. Your family deserves stability. Your health deserves proper care without the shadow of financial ruin hanging over every decision.

Get the coverage right. Get it right today. Because the one thing guaranteed about a medical emergency is that it will never arrive at a convenient time, and it will never politely wait until your insurance is in order.